As the Federal Government moves its policy focus beyond COVID-19 economic survival, to economic revival, new laws in the form of the Payment Times Reporting Act 2020 have been passed which will attempt to improve the payment practices of large businesses in Australia.

Large businesses will need to publicly report on their small business payment practices

The Payment Times Reporting Act 2020 (Cth) (Cth) requires all large businesses with annual turnover greater than $100m, including corporate groups which exceed that turnover, to submit a payment times report twice each reporting year, to a newly created Payment Times Reporting Regulator.

That report will be in a standard form and be required to include specific information about the payment terms and practices of the submitting business, based off of actual payment data, and will include, amongst other requirements, reporting on:

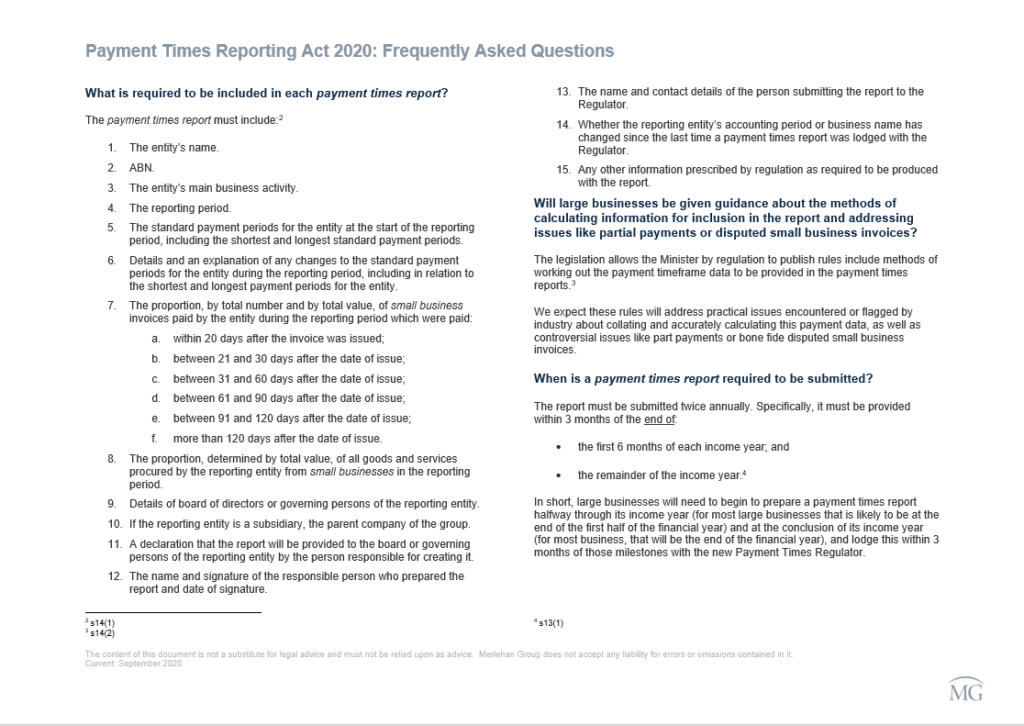

- The standard payment periods for the entity at the start of the reporting period, including the shortest and longest standard payment periods.

- Details and an explanation of any changes to the standard payment periods for the entity during the reporting period, including in relation to the shortest and longest payment periods for the entity.

- The proportion, by total number and by total value, of small business invoices paid by the entity during the reporting period which were paid:

- within 20 days after the invoice was issued;

- between 21 and 30 days after the date of issue;

- between 31 and 60 days after the date of issue;

- between 61 and 90 days after the date of issue;

- between 91 and 120 days after the date of issue;

- more than 120 days after the date of issue.

- The proportion, determined by total value, of all goods and services procured by the reporting entity from small businesses in the reporting period.

This information will then be uploaded onto an online free and publicly accessible Payment Times Register. This register will allow small businesses and members of the public (and press) to freely interrogate the payment practices of large businesses, and in the case of small businesses, make better informed decisions about who to do business with.

Large businesses will be required to keep records of information used to prepare these payment times reports for at least 7 years after the report is submitted.

The laws are aimed at improving large business payment practices in Australia by exposing large businesses’ payment practices to greater public scrutiny and allowing small businesses access to reliable information on payment practices of their potential customers

The theory behind the new laws is that long and late payment times adversely affect the cash flow of small businesses, leading to higher bankruptcy and exits rates, and small businesses lack the market power to correct this issue. The Federal Government has concluded that new laws are required to effect cultural change to payment practices of large Australian businesses, which will in turn deliver economic benefit to the Australian economy.

The Federal Government estimates that the net benefit to small business from normalising small business payment times to 30 days would be $522 million per year, with an estimated net benefit to the Australian economy of $313 million per year.

The goal of the new laws is to see large businesses in Australia adopt more reasonable payment terms, of shorter duration, when paying small businesses.

Civil penalties and enforcement powers will apply to compel compliance by large businesses with these new laws

The Payment Times Reporting Regulator may publish the identity of entities who fail to comply with the Act to publicise that misconduct.

Additionally, after a grace period of 12 months from commencement of these new laws, civil penalties of up to 0.6% of a large business’ annual turnover may apply to large businesses who fail to comply with these new laws.

The Regulator will also be given broad audit, monitoring and investigation powers under the Act including rights of entry, inspection, search and seizure of evidence to investigate and prosecute non-compliance with these new laws.

Where the Payment Times Reporting Regulator reasonably suspects that a reporting entity has breached these new laws, the Payment Times Reporting Regulator will also be able to force large business to engage, at the large business’ expense, an independent auditor to audit compliance with these laws and provide a report of the auditor’s findings to the Regulator.

The new laws commence 1 January 2021*

The commencement date for the new laws is 1 January 2021*.

*However, if a reporting entity’s income year started in the 6 months prior to 1 January 2021 (as would be the case for reporting entities with income years aligned with the financial year), the first 6 months of that income year is excluded as a reporting period under the Act, and the entity is only required to submit its first payment times report within 3 months from the end of that reporting entity’s income year.1s54A

Key takeaways – develop a compliance program now

Large businesses in Australia should begin preparing amendments to their corporate compliance programs and finance functions now in readiness to comply with these new laws.

We also recommend C-suite consideration be given to how current payment practices are likely to compare with industry and competitors when they published on the new public register. This should be done to determine whether reputational risk to brand could arise as a consequence of these new laws and the public scrutiny they will facilitate, conversely, whether any opportunity can be seized by drawing upon data to be published on the Payment Times Reporting Register by highlighting excellent payment practices, improving brand and reputation in the process.

We are currently supporting large businesses to navigate compliance with these new laws through our leading legal expertise, financial analytics expertise from our corporate financial analytics consultants and marketing strategy guidance from our senior marketing strategy consultants.

For support across one or more of these domains to ensure your business properly engages with the task of complying with these new laws, please contact our Adam Merlehan.

Frequently asked questions

Some of the finer details of how these new laws will apply, and the questions they are likely to raise for business executives tasked with implementing them in the more than 3,000 large businesses and government owned enterprises affected by these new laws are addressed in the FAQs which can be clicked on below for download and review.

Author

References

| *1 | s54A |

|---|